California’s State Appropriations Limit (Gann Limit)

California’s State Appropriations Limit (SAL)—commonly known as the Gann limit—is a constitutional cap on how much tax revenue the state government can spend each year. The rule was created by voters through California Proposition 4 (1979), largely championed by anti-tax activist Paul Gann. It was later significantly modified by California Proposition 111 (1990). Together, these measures established a formula that restricts spending growth based on factors such as population and inflation.

The purpose of the Gann limit is to prevent state government spending from expanding faster than the economy and population. The limit applies to spending from tax proceeds, not to federal funds or certain other revenues. Importantly, local governments must also comply with their own appropriations limits under the same constitutional framework.

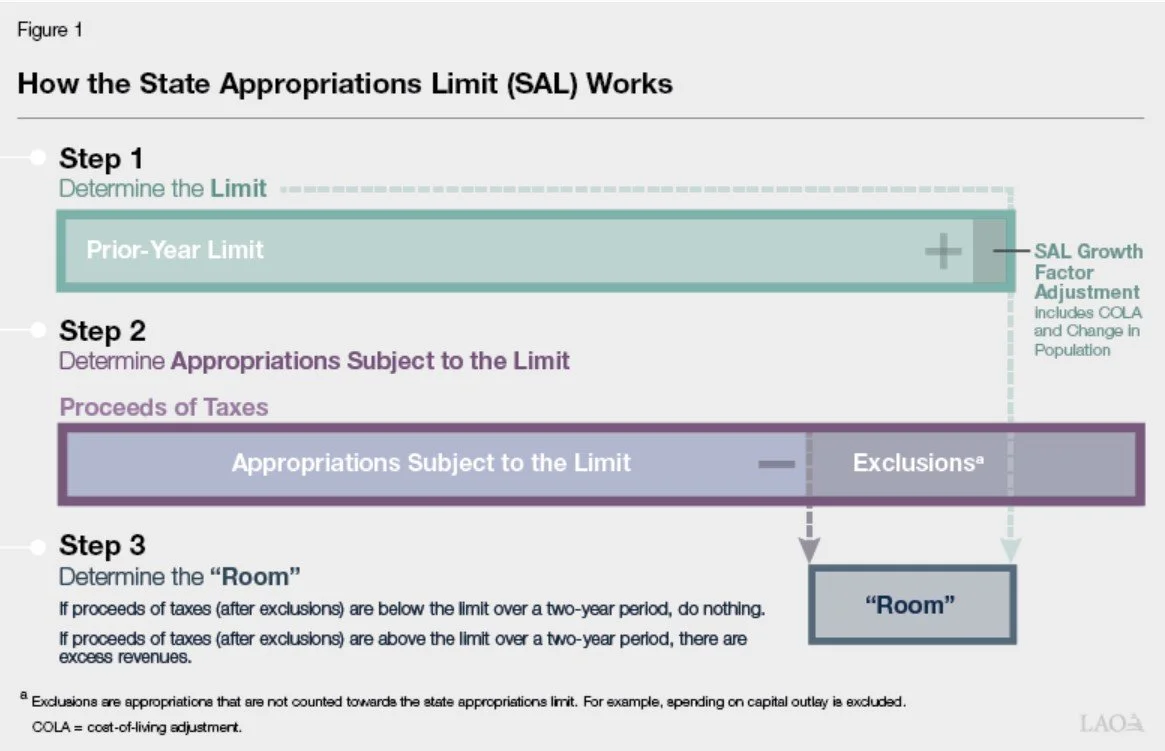

If California exceeds the limit for two consecutive years, the state cannot simply continue spending the additional revenue as it wishes. Instead, the excess must be redirected in specific ways. The money must either be returned to taxpayers, distributed to schools, or spent on certain allowable one-time purposes such as infrastructure projects or payments to local governments. See LAO figure #1 below.

As of the state budget projection released on January 9, 2026, California remains below the spending cap. Current estimates show the state about $6.5 billion under the limit in 2024–25, $21.2 billion under in 2025–26, and $33.8 billion under in 2026–27. However, stronger-than-expected tax revenues—or new taxes—could bring the state closer to the limit in the coming years.

Approaching the Gann limit has important implications for the state budget. Higher revenues can automatically increase spending obligations in certain areas, particularly funding for K–12 schools under California Proposition 98 and deposits into state reserves under California Proposition 2 (2014). If the limit is actually reached, lawmakers have less flexibility in how they allocate additional revenue.

To stay within the constitutional cap, the state may need to redirect funds or reduce spending in programs that are not constitutionally protected. These could include areas such as health and human services, housing programs, universities, corrections, and natural resource initiatives.

A recent example occurred in 2022, when California redirected roughly $48 billion in surplus funds toward allowable one-time spending—such as infrastructure—and issued $9.5 billion in taxpayer refunds to avoid exceeding the limit.

While the Gann limit plays a major role in shaping California’s fiscal policy, it does not account for structural deficits or potential federal funding reductions. As revenues fluctuate, policymakers must continue balancing constitutional spending limits with the state’s growing needs.